A Fundamentals-Driven Market Emerges (2026 Outlook)

Q1 2026 Dynamics

The net lease market has finally moved past the noise of the last few years and is settling into something much healthier. Reality. After a stretch where everyone was trying to outguess the Fed and justify pricing off headlines instead of fundamentals, we’re back to underwriting deals the way they’re supposed to be underwritten. Transaction velocity is returning, pricing has stabilized, and more importantly, buyers are showing up with intent. This isn’t a “hot” market, and it’s definitely not a broken one. It’s a smart market. Private capital and REITs are re-engaging, bid-ask spreads are tightening, and deals are getting done, particularly in retail and industrial. But unlike prior cycles, not everything trades the same. Performance is being positively driven by tenant quality, lease structure, real estate fundamentals, and replacement cost. We expect transaction volume to increase 15–20% in 2026, but it will be driven by conviction, not momentum.

Is CRE Cheap?

At the same time, something bigger is happening under the surface that isn’t getting enough attention; commercial real estate is now “cheap” relative to equities for the first time in over 20 years. That’s not a headline we’ve seen in two decades, with cap rates relative to stock market P/E ratios having flipped in favor of real estate. While equities continue to ride a wave of optimism, much of it tied to AI and future growth narratives, CRE is quietly sitting there as a value play. Liquidity pressure is easing, bid-ask spreads are narrowing, price discovery is improving, and private values are projected to increase roughly 5% in 2026. In other words, the reset may have already happened.

For investors looking around and thinking stocks feel a little crowded, expensive, and too reliant on “what could be,” real estate, specifically net lease, is remerging as a disciplined alternative. Durable income, risk-based pricing already baked in, stable fundamentals in necessity-based retail, and attractive cash-on-cash yields in a still elevated rate environment make it a pretty compelling place to be. Capital hasn’t fully returned yet, and that’s exactly why this window matters. The best opportunities rarely come when everyone agrees.

The Confidence Trend

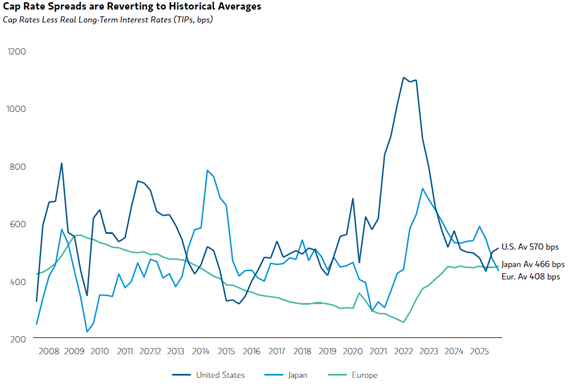

One of the biggest shifts in today’s market is the move away from treating net lease like a bond proxy. For years, deals were priced off the 10-year Treasury plus a spread, and that was extent of the analysis. Today, that approach will get you into trouble. Cap rates have stabilized, not because rates have come crashing down, but because investors have regained confidence in how to actually price risk. There’s now real differentiation between tenants, locations, and real estate quality. Investors are now asking the questions that have always mattered; who is the tenant, why are they in this location, and what happens when the lease expires? That last question, which was largely ignored during the frothier years, is now front and center.

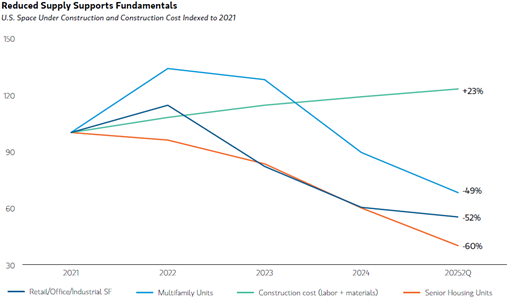

Another major force supporting the market right now is the disconnect between construction costs and achievable rents. At the same time, rents in many sectors are still roughly 20% below what’s needed to justify new development. The result is a slowdown in new construction and a meaningful reduction in supply. That dynamic is quietly doing a lot of heavy lifting for existing assets. If it doesn’t make sense to build today, then what already exists becomes more valuable by default. Capital is flowing toward stabilized assets, functional buildings, and locations that would be difficult to replicate. Until rents catch up or construction costs come down in a meaningful way, that supply constraint will continue to support valuations.

A Normalized Capital Market

Capital markets are also reopening, but with discipline. Lenders are back, but they’re underwriting deals, not stories. Equity is active, but selective. At the same time, the market is working through a significant maturity wall, with roughly $875 billion to $1 trillion of commercial real estate debt coming due in 2026. That creates both pressure and opportunity. Some assets will need to be refinanced in a tougher environment, others will trade because they must, and many will be recapitalized. For investors who are prepared, this isn’t a problem, it’s inventory. Sale-leasebacks, structured transactions, and recap opportunities are all likely to increase as a result. Liquidity is returning, but it’s no longer being handed out freely. It must be earned through good real estate and strong execution.

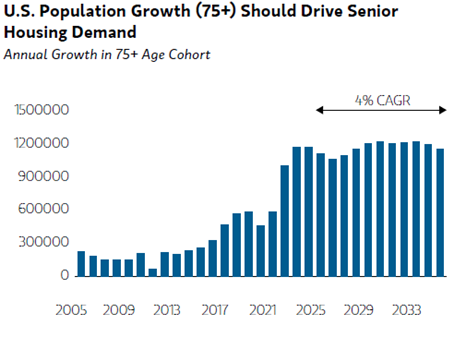

From a sector standpoint, industrial remains a strong performer, but it’s no longer a rising tide lifting all boats. Supply has pulled back to near 15-year lows, and while leasing activity remains healthy, investors are being far more selective. The focus has shifted to functionality, location, and tenant use. The days of buying anything with a loading dock and assuming it will work itself out are over. At the same time, senior housing continues to benefit from long-term demographic trends that are hard to argue with. An aging population, increasing need for specialized housing, and improving funding mechanisms are creating a durable foundation for growth. Unlike other sectors that rely heavily on economic cycles, this one is supported by something much simpler. Time.

For investors, the takeaway is straightforward. This is no longer a market about chasing yield compression or relying on momentum. It’s about buying the right deal. The groups that will win in 2026 are the ones focused on durability of income, real estate optionality, and basis relative to replacement cost. It’s about understanding not just what the asset is today, but what it could be tomorrow. The biggest mistake right now is still thinking there is a “market price” for everything. There isn’t. Pricing is increasingly buyer-specific, and understanding who the right buyer is, and how they think, is more important than ever.

Conclusion

After several years of uncertainty, the net lease market has reset. That’s not a negative, it’s exactly what needed to happen. What we’re seeing now is the beginning of a more rational, fundamentals-driven cycle. More transactions, more discipline, and more differentiation between good deals and bad ones. This next phase won’t be defined by easy money or aggressive compression. It will be defined by execution, underwriting, and a real understanding of value.

At SAB Capital, that’s where we operate. We don’t believe in pushing deals, we believe in understanding them. The asset, the tenancy, and the buyer. Because at the end of the day, the market doesn’t pay for what something is, it pays for what it solves.

If you’re interested in understanding how your tenancy is valued in this evolving interest rate environment and how it can be used more effectively to accomplish your investment or portfolio management goals, please reach out to our transaction professionals.